The Rule of 72 is a handy, easy-to-use tool within the DividendFarmer’s toolbox. It’s perfect for quickly ball-parking the time

required for your investment to grow to your desired level. For

instance, you may ask yourself, “Self, if I have a $10,000 dividend portfolio

with a 4% yield, how long will it take for my money to double?”

The Rule of 72 is a handy, easy-to-use tool within the DividendFarmer’s toolbox. It’s perfect for quickly ball-parking the time

required for your investment to grow to your desired level. For

instance, you may ask yourself, “Self, if I have a $10,000 dividend portfolio

with a 4% yield, how long will it take for my money to double?”

If you're familiar with the Rule of 72, you’ll know that at 4%,

your money will double in about 18 years. But what if your portfolio

is paying 6%? Then your money will double in roughly 12

years. What if your portfolio is paying a meager 2%? Then

36 years is the general length of time needed to double your money, left to its

own devices.

So how does this Rule of 72 work? How can you quickly

determine the length of time needed for your money to double based only upon

the dividend yield of your stock? Investopedia explains the Rule of 72 in mathematical

terms. If you understand logarithmic functions, the explanation hits

the spot.

However, if you’re like this Dividend Farmer, you may want a less

technical explanation which starts with the principle of compound

interest. If you invest $1 today at 7%, compounded annually over

several years, you will have a progression that looks something like the table

below.

Start

|

Year 1 (end)

|

Year 2 (end)

|

Year 3 (end)

|

Year 4 (end)

|

Year 5 (end)

|

Year 6 (end)

|

Year 7 (end)

|

Year 8 (end)

|

$1.00

|

$1.07

|

$1.14

|

$1.22

|

$1.31

|

$1.40

|

$1.50

|

$1.60

|

$1.71

|

At the end of year 8, your investment will have grown by $.71 or

71%. This doesn’t sound like much, but it’s only a dollar and you

didn’t add anything to it. You simply waited and watched it grow

much like traditional farmers do with their crops.

Using the principle of compounding and applying the

aforementioned logarithmic function, an ingenious little formula was developed,

called the Rule of 72, allowing you to closely

approximate the length of time needed to double your money for a given interest

rate.

Behold the magic formula: 72 / interest

rate (or yield) = years to double.

Using an earlier example of 6% and applying the Rule of 72

results in the following: 72 / 6 = 12 years to

double. It’s that easy.

The best part is that you can work the formula back and forth

using basic algebra to find out what interest rate is required for your money

to double in a given number of years. For instance, if I want my

money to double in 10 years, what interest rate do I need to earn on my

investment?

If 72 / x = 10 years then 72 / 10 equals 7.2. This

conversion actually requires a little cross multiplication, then division to

put x in the right place, but it works! I need to earn 7.2%,

compounded annually, for my money to double in 10 years.

It’s not uncommon for me to contemplate the length of time it

might take a dividend stock I’m investigating to double in value based upon its

dividend yield. I use the Rule of 72 when I do. And when I had

a longer time horizon, I used the formula to determine how much money I might

have after a 40 year work period assuming a specific interest rate compounded

annually. By-the-way, this exercise is great for fresh college grads

or industrious high schoolers as well.

For instance, after 40 years of compound interest at 4% starting

with $10,000, I quickly estimated I would earn in the neighborhood of

$50,000. My napkin math went something like this. At 4%,

my money doubles in 18 years becoming $20,000. In another 18 years

(36 total) it will double again to $40,000 and I’ll still have 4 years left of

the original 40. Those 4 years represent almost 25% of a third 18

year period-to-double in which case I should see close to 25% of the $40,000

added to it during those 4 years. Consequently, I expected to see

the figure grow to approximately $50,000. Using Excel and the Future

Value (FV) formula, which we’ll talk about in another post, I can work the same

problem to discover my actual earnings will be $48,010.21. Not bad

for ballpark, eh?

Some caveats are in order at this point.

First, the Rule of 72 works well until you begin talking about

very large interest rates e.g., north of 50%. However, investment

returns of that scale are infrequent and probably warrant a healthy dose of

caution if ever presented to you. Better yet, run away.

Second, the Rule of 72 works best when investments are

compounded on an annual basis. For dividend paying stocks that

distribute quarterly or monthly, the approximation given by the Rule of 72 may

be slightly farther off the mark, but not so far as to be of no value.

Third, the Rule of 72 doesn’t account for additional payments

you make to your investment portfolio during the compounding

period. To calculate the size of your nest egg at retirement,

including compound interest and infusions of money into your investment basket

for example, you’ll need to use the Future Value formula in Excel I mentioned

earlier.

Fourth, and very importantly, the Rule of 72 is applicable when

discussing compound growth rates – thus the heavy use of the words “compound”

or “compounding” in this post. Some financial advisors may try to

bamboozle you with the Rule of 72 and average rates of return which can be VERY

different from the compound growth rate used as the foundation for the Rule of

72. The compound growth rate and average rate of return are different

beasts and will be discussed in another post.

There you have it. The Rule of 72. It took

longer for me to explain than it will for you to use once you get the hang of

it, but it’s a simple, invaluable tool in the Dividend Farmer’s

kit. That’s why The Rule of 72 “Rules”.

The thoughts and opinions

expressed here are those of the author, who is not a financial

professional. Opinions expressed here should not be considered investment

advice. They are presented for discussion and entertainment purposes

only. For specific investment advice or assistance, please contact a

registered investment advisor, licensed broker, or other financial

professional.

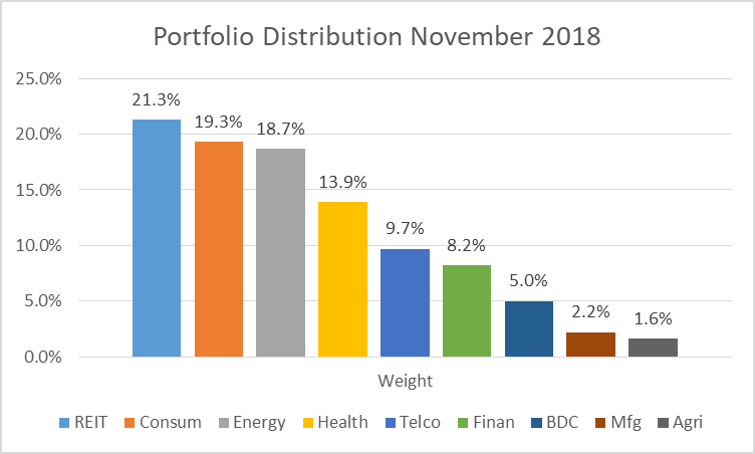

In monitoring news articles and blogs no issues were found to

be overly concerning regarding my holdings.

Once again, I’m not checking ticker symbols on a regular basis since my

focus is on building the dividend income stream rather than market value. Consequently, I try to focus on substantive

issues adversely affecting the abilities of the investments to generate cash and

didn’t find any in headline.

In monitoring news articles and blogs no issues were found to

be overly concerning regarding my holdings.

Once again, I’m not checking ticker symbols on a regular basis since my

focus is on building the dividend income stream rather than market value. Consequently, I try to focus on substantive

issues adversely affecting the abilities of the investments to generate cash and

didn’t find any in headline.